Surveys of company executives indicate that their number problem with ESG is the multitude of partially conflicting and overlapping reporting frameworks and regulations: one estimate puts the number of ESG reporting frameworks at 600 worldwide. Another source, the healthcare, tax and accounting consultancy Wolters Kluwer, lists ‘multiple ESG frameworks’ as among the five biggest hurdles to effective ESG reporting.

But things might be slowly taking a turn for the better, partially as a result of investors pushing for more uniform and financially relevant ESG standards.

Responding to investor pressure

A response came last summer from the accounting standards organization IFRS and its subsidiary the International Sustainability Standards Board (ISSB), which launched its sustainability standards IFRS S1 and S2. Voluntary S1 and S2 reporting started January 1, 2024 in various jurisdictions, and will become mandatory a year or so later, depending on the country in question.

One of the stated aims of IFRS S1 and S2 is to incorporate the most relevant standards of existing frameworks into a single global standard, and to provide investors with data connecting ESG and financial risk or return in companies.

In explaining the rationale for the new standards, ISSB cites a survey showing that investors’ number one motive for committing capital to ESG is ‘financial performance’, named by 74 percent of respondents to a Morgan Stanley investor survey.

IFRS traditional accounting standards are used in 140 jurisdictions worldwide. The body’s apparent aim is to generate a similarly broad acceptance for its ESG standards, S1 and S2. More than 20 countries have currently endorsed or will require them.

Consistent with IFRS’ focus on company accounting, S1 and S2 are so-called single-materiality standards: in other words, they cover ESG impacts on companies. Many other frameworks are double-materiality, reporting impacts both on companies and the macro environment.

On the surface, S1 and S2 look easy and flexible, enabling a more financially relevant approach to ESG reporting:

- S1 focuses on all sustainability-related risks and opportunities that could reasonably be expected to impact companies’ cash flow, access to finance or cost of capital in the short, medium and long term

- S2 specifies disclosures related to climate and is intended to be applied together with S1.

In practice, the standards are complex yet structured and logical and allow companies to report data adjusted to their jurisdictions and sectors. The multitude of documents, webinars and levels of IFRS membership reveal that the standards are – at least initially – not so easy, however.

Can they improve the ESG reporting muddle?

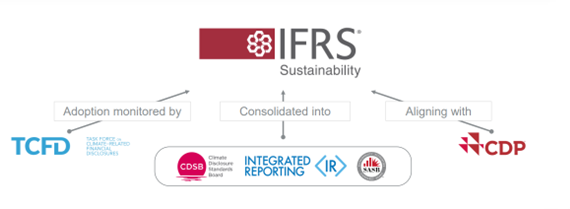

IFRS S1 and S2 claim not to have reinvented the wheel, so as not to contribute to the current confusion. They are built on the framework and standards of the International Accounting Standards Board, TCFD, SASB and Climate Disclosure Standards Board and collaborate with the GRI – all established frameworks. S1 and S2 are also intended to align with current and upcoming regulations worldwide, reducing the reporting burden on companies.

The aim is to ‘inter-operate’ with other standards. That is, if companies report according to any of the existing major frameworks, they’ll find it easier to adopt S1 and S2.

Yet they are not just a synthesis of existing standards, nor are they a mere collection of facts and figures. The ‘materially relevant’ performance data reported under S1 and S2 have the taste of financial reporting, and are supposed to be presented in regular financial reports alongside financial data.

Indeed, S1 and S2 look very much like SEC 10K or 20F filings, emphasizing actionable data that investors need to decide on providing capital and resources to companies, buying/selling equity and debt and engaging in active governance.

Accordingly, they emphasize the following elements:

- Comprehensive descriptions of all interrelated links that may impact company performance, ranging from macro risks (such as economic downturns or climate change) to micro risks (such as debt, cyber-security or liquidity)

- Opportunities, such as impact on equity value brought about by a stream of ESG-friendly products, for example

- Strategies and processes that companies have in place or are instituting to reduce risks, reinforce opportunities and thus improve financially relevant performance

- Quantitative data demonstrating how ESG efforts are impacting key financials such as revenues or cost of capital

- Projected performance data, including historic and projected greenhouse gas data and how these could be linked to reducing the risk of fines by regulators, for example

- Flexibility in calculating data and, if companies cannot yet quantify all impacts, descriptions will do.

In conclusion, IFRS S1 and S2 are likely to succeed as a global reporting framework because they encompass actionable data, meet investor needs and use a more financial reporting structure that companies are used to.

Dr William Cox is CEO of Yieldrive, a fintech in Switzerland specializing in calculating ESG in dollars and cents

William Cox

Dr William Cox is CEO of Yieldrive, a Fintech in Switzerland specializing in calculating ESG in Dollars & Cents. Cox has spent 20 years focusing on the financial impacts of ESG on companies. He received his PhD from the London School of Economics, a...